Managerial Accounting Which Is the Best Definition of a Standard

Here are six ways to differentiate management accounting vs. Basic standards are seldom revised or updated to reflect current operating costs and price level changes.

Compare Managerial And Financial Accounting Google Search Accounting Education Managerial Accounting Cost Accounting

Managerial accounting also called management accounting is a method of accounting that creates statements reports and documents that help management in making better decisions related to their business performance.

. The budget for a single unit of product. The Chartered Institute of Management Accountants UK defines a basic standard as the standard which is established for use unaltered for an indefinite period which may be a long period of time. Management accounting is a modern concept of accounting as a tool of management.

These standards are based on perfect or ideal conditions and do not allow any room for any poor-quality raw materials waste in production or other inefficiencies. Managerial accounting is intended for internal administrators of a business to make internal decisions. Strategy using the insight from analysis to help formulate business strategy to create wealth and shareholder value.

Financial accounting on the other hand deals with financial records intended for external actors such as investors creditors or lenders. This approach represents a simplified alternative to cost layering systems such as the FIFO and LIFO methods where large amounts of. Management accounting is essential for an organization to be better equipped and control functions.

Managerial accounting focuses on operational reporting and looks to the future by using forecasting. Managerial accounting is primarily used for internal purposes. In contrast financial accounting is for both internal and external stakeholders.

Financial accounting is mainly for the purpose of informing outside parties shareholders lenders creditors and government. Managerial accounting is part of the accounting job where this function focuses more on recording managing and analyzing the cost of products or services in an organization. Risk applying.

In addition to strong accounting fundamentals CIMA teaches strategic business and management skills. Management accounting provides managers with necessary information to make informed business decisions. In a standard costing system standards are normally categorized as ideal standards and practical standardsThe difference between these two types of standards is briefly explained below.

An accounting standard is a set of practices and policies used to systematize bookkeeping and other accounting functions across firms and over time. Managerial accounting is designed for an internal audience and the general public doesnt read the reports or statements that management accountants produce. Standard Costs Variances.

CVP is one of the most basic planning tools available to management and is a key step in decision making by many firms. Unlike financial accounting which is designed for external users managerial accounting is focused on internal managers. Managerial Accounting Chapter 11.

Management accounting is the process of identification measurement accumulation analysis preparation interpretation and communication of information that assists executives in fulfilling organizational objectives. Management vs financial accounting. Managerial accounting is the process of identifying analyzing interpreting and communicating information to managers to help managers make decisions within a company and to help achieve business goals.

Managerial accounting reports are issued more frequently and follow no specific period. Accounting standards apply to the full breadth. It aims to provide external parties with information about the financial health of a business.

OThis type of standard is best suited for companies that strive for. Standard costing is the practice of substituting an expected cost for an actual cost in the accounting records. The ICMA London has defined management accounting as the presentation of accounting information in such a way so as to assist management in the creation of policy and in day to day operations of an undertaking.

Managerial accounting is designed to help managers plan for the future make decisions for the company and determine if their plans and decisions were accurate also called controlling. Subsequently variances are recorded to show the difference between the expected and actual costs. Managerial accounting is the practice of identifying measuring analyzing interpreting and communicating financial information to managers for the pursuit of an organizations goals.

Management Accounting Definition The management accounting definition is accounting with the specific purposes of informing managers. Management accounting also is known as managerial accounting and can be defined as a process of providing financial information and resources to the managers in decision making. Basically managerial accounting is the same as management accounting.

These reports are shared internally within the company typically with managers and senior employees. This can also be known as cost accounting. Management accounting deals with the use of accounting information to managers within an organization.

Importance of managerial accounting. Analysis understanding the story behind the numbers and using it to make business decisions. Ideal standards are standards that do not allow for normal wastage and work interruption due to breakdown of machinery employees rest periods.

CVP analysis involves specifying a model of the interrelationships among selling prices of products volume or level of activity unit variable costs total fixed costs mix of products sold and operating income to help. One simple definition of management accounting is the provision of financial and non-financial decision-making information to managers. In other words management accounting helps directors inside an organization to make decisions.

Management accounting is only used by the internal team of the organization and this is the only thing which makes it different from financial accounting. It helps the management to perform all its functions including planning organizing staffing direction and control. These two terms mean the same thing.

Cost Costing Cost Accounting And Cost Accountancy Cost Accounting Accounting Accounting Student

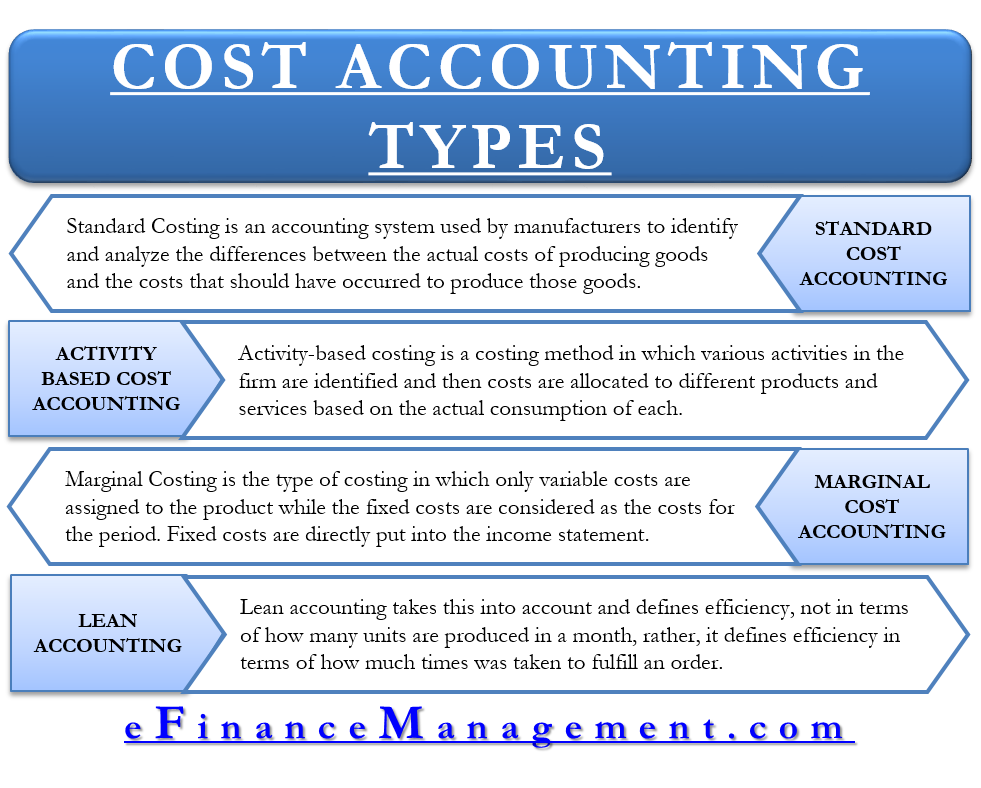

Types Of Cost Accounting Standard Activity Based Marginal Lean Efm

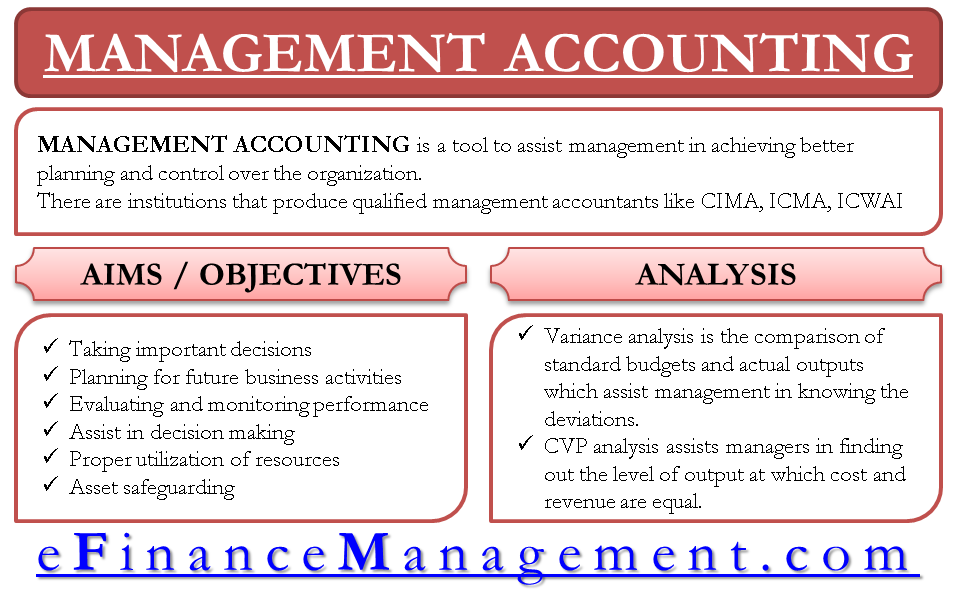

Management Accounting Define Aim Budget Variances Cvp Analysis

Comments

Post a Comment